INDONESIA’S DIGITAL REVOLUTION: HOW 351 MILLION SMARTPHONES ARE RESHAPING A NATION’S FUTURE

INTRODUCTION: THE SMARTPHONE PHENOMENON THAT TRANSFORMED A NATION

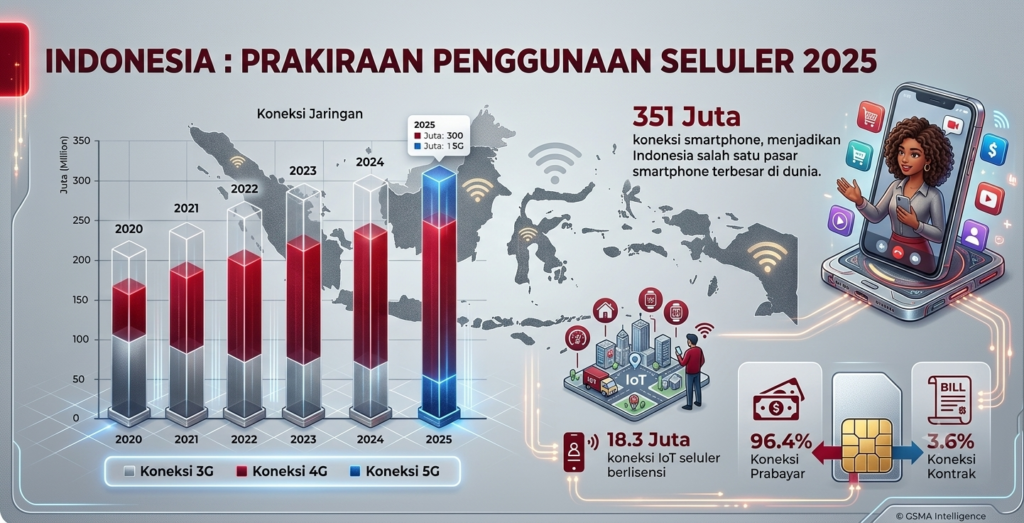

Indonesia stands at the nexus of a remarkable transformation: 351 million smartphones connecting Indonesians to the digital world, making the nation the world’s largest smartphone market—a distinction that carries profound implications for economic development, social connectivity, and the future of digital commerce across Southeast Asia.

This extraordinary penetration of mobile technology in Indonesia is not merely a commercial phenomenon or a measure of consumer device ownership. It represents a fundamental restructuring of how Indonesians access information, conduct commerce, maintain relationships, pursue education, and participate in democratic processes. The mobile phone, in Indonesia’s context, has become more than a communication device—it has become the primary gateway to the digital economy, to financial services, to educational opportunities, and to participation in the modern world.

As of June 2026, the latest data from GSMA Intelligence reveals a telecommunications landscape transformed by rapid technological advancement, aggressive infrastructure investment, and evolving consumer behavior. The comprehensive statistics paint a portrait of a nation simultaneously navigating the opportunities and challenges of digital transformation at unprecedented scale.

1. THE SCALE AND SIGNIFICANCE OF INDONESIA’S SMARTPHONE MARKET

1.1 A Global Market Leader

Indonesia has achieved a remarkable distinction: 351 million smartphone connections, making Indonesia the world’s largest smartphone market—larger than the United States, larger than Europe, larger than any single nation on Earth.

This statistic, while impressive, demands careful interpretation. The 351 million figure represents connections rather than unique individuals. Many Indonesians maintain multiple devices; some maintain multiple subscriptions on a single device. Nevertheless, the raw number reflects the extraordinary penetration of mobile technology across Indonesian society.

To contextualize this number: Indonesia’s total population stands at approximately 270 million. The fact that smartphone connections exceed population by nearly 100 million indicates extraordinary market saturation. Multiple devices per individual, subscriptions maintained across family members, and devices retained by users after upgrades all contribute to this dynamic.

1.2 The 96.4% Mobile Connectivity Penetration Rate

Even more remarkable than the absolute number of smartphones is the penetration statistic: 96.4% of mobile connections in Indonesia now utilize “broadband” connectivity—meaning connections via 3G, 4G, or 5G mobile networks.

This figure represents a dramatic transformation from earlier eras when basic 2G cellular technology dominated Indonesia’s telecommunications landscape. The progression visible in GSMA data—from 3G dominance in 2020 to increasingly robust 4G and emerging 5G infrastructure by 2026—illustrates the pace of technological transformation.

The 96.4% broadband penetration rate indicates that nearly all mobile connections in Indonesia now theoretically support data transmission at speeds and capacities far exceeding those available through older 2G and 3G technologies.

1.3 Mobile-First Digital Access

The dominance of mobile connectivity in Indonesia reflects global patterns evident across developing and developed economies: the mobile phone has become the primary—often the only—device through which hundreds of millions of people access the internet.

For many Indonesians, particularly in rural areas or lower-income urban neighborhoods, the smartphone represents their sole connection to digital services. Rather than progressing through stages of digital adoption—first desktop computers, then laptops, then tablets, finally smartphones—many Indonesians adopted mobile phones as their first and primary digital device.

This “mobile-first” path to digital access creates distinctive patterns of digital behavior: Indonesian internet usage emphasizes social media, messaging applications, and mobile-optimized services. Websites designed for desktop computers often prove frustrating to Indonesian mobile users, driving demand for mobile-native applications and services.

2. THE TELECOMMUNICATIONS INFRASTRUCTURE UNDERPINNING SMARTPHONE ADOPTION

2.1 The 4G Revolution: Coverage and Dominance

4G services accounted for a majority share of the overall mobile subscriptions in 2024 in Indonesia and will remain the leading mobile technology through 2029, according to GlobalData analysis.

The dominance of 4G reflects a strategic decision by Indonesia’s major mobile operators to deploy 4G infrastructure broadly across the archipelago. Despite Indonesia’s geographic challenges—an archipelago of over 17,000 islands spread across a geographic region vast as continental Europe—major operators achieved impressive 4G coverage:

- Telkomsel: Over 97% population coverage for 4G as of December 2024

- Indosat: Significant 4G coverage supporting 95 million subscribers in Q3 2025

- XL Axiata and Others: Substantial 4G infrastructure supporting competitive markets

This 4G dominance has created a foundation for mobile internet services, with implications visible in Ookla’s speed measurements: Indonesia’s median mobile internet download speed increased by 15.61 Mbps (+53.1 percent) in the twelve months to August 2025.

1.2 5G Emergence and Expansion

While 5G is at the start of its journey in Indonesia, the ambitious plans of the government and operators means that more than 32% of connections are expected to run over 5G by 2030, according to the GSMA Intelligence report.

Early 5G deployment has focused on major urban centers and commercial hubs. By mid-2025, Telkomsel operated over 3,000 5G base stations across 56 cities. Recent expansions in June 2025 extended 5G coverage in Batam by deploying additional 5G base transceiver stations (BTS) in key areas of the city, taking the total BTS units to about 112 and improving 5G connections in key commercial and residential areas like Harbour Bay, Nagoya, Batam Center, Engku Putri and Hang Nadim Airport.

The progression from 3G (2020) to robust 4G (2024-2025) to emerging 5G (2025-2026) visible in GSMA data shows infrastructure evolution driven by:

- Operator Investment: Telkomsel, Indosat, XL Axiata, and others collectively investing approximately $18 billion between 2024 and 2030 to support advanced connectivity

- Spectrum Allocation: Government spectrum auctions and allocations enabling operators to deploy next-generation networks

- Device Availability: Expanding availability and falling prices of 5G-capable smartphones making next-generation connectivity accessible to broader consumer segments

- Consumer Demand: Rising demand for higher-speed, higher-capacity mobile services driving operator investment

1.3 5G Adoption Projections

GSMA forecasts indicate that 5G could account for more than 30 percent of mobile connections in Indonesia by the end of the decade. Some 67% of connections will be 4G by 2030, with 94% of people using smartphones, according to GSMA projections.

This forecast suggests continued 4G dominance through the 2020s while acknowledging accelerating 5G adoption. The coexistence of 4G and 5G technologies reflects technological realities: operators maintaining 4G networks for broader geographic coverage while deploying 5G in urban areas and commercial hubs where data demand justifies infrastructure investment.

3. THE MOBILE OPERATOR LANDSCAPE: COMPETITION AND CONSOLIDATION

3.1 Telkomsel’s Market Leadership

Telkomsel remained Indonesia’s largest mobile operator in Q3 2025, leading the market in both ARPU (Average Revenue Per User) and subscriber base. The company reported an ARPU of IDR 43,400, the highest in the industry, despite a slight decline in subscribers to 157.6 million.

Telkomsel’s market leadership reflects several competitive advantages:

- Network Coverage: Achieving over 97% population coverage with 4G services

- 5G Infrastructure: Operating the most extensive 5G network among Indonesian operators, with plans for continued expansion

- ARPU Optimization: Achieving the highest average revenue per user through premium service packages and customer mix optimization

- Strategic Rationalization: Deliberately reducing low-cost subscriber segments to focus on higher-value customers, supporting stronger monetization

3.2 Indosat’s Strategic Evolution

Indosat achieved a long-standing strategic target by reaching an ARPU of IDR 40,000 in Q3 2025, supported by network improvements and customer mix optimization. The operator served 95 million subscribers during the period.

Indosat’s evolution represents a competitive response to Telkomsel’s dominance and reflects industry-wide trends toward premium service positioning. By focusing on higher-value customers and emphasizing network quality improvements, Indosat competes not primarily on price but on service quality and customer experience.

3.3 Market Structure and Regulatory Context

Indonesia’s mobile telecommunications market features a competitive structure with multiple national operators (Telkomsel, Indosat, XL Axiata, and others) competing across different customer segments and geographic regions.

The regulatory environment has historically presented challenges to efficient operator investment. Annual spectrum fees represent more than 12% of recurring revenues—above the APAC median of 8.7%—creating financial burdens on operators. Past spectrum auctions resulted in fragmented spectrum holdings, impacting spectral efficiency and increasing costs.

However, encouragingly, the government’s 2025–2029 digital roadmap addresses many of these issues through:

- Reduced 5G Spectrum Fees: Proposing reduced fees for 5G spectrum (no more than 50% of 4G rates)

- Rural Deployment Incentives: Offering incentives for rural deployments tied to more affordable spectrum access

- Regulatory Modernization: Modernizing the regulatory environment to enable more efficient network investment

4. MOBILE DATA SERVICES: THE GROWTH ENGINE OF TELECOMMUNICATIONS REVENUE

4.1 The Shift From Voice to Data

Mobile voice service revenue will decline during the forecast period, due to the free bundling of voice minutes by mobile network operators into their mobile plans, rising user preference for OTT (Over The Top) internet communication services like WhatsApp, Telegram, and Viber, and the subsequent decline in mobile voice ARPU levels.

This transition from voice-centric to data-centric telecommunications reflects global patterns: as internet-based communication services (messaging, voice over IP, video calling) become standard, traditional cellular voice services decline in importance and revenue significance.

4.2 Mobile Data Revenue Growth

Mobile data service revenue, on the other hand, will continue to increase at a healthy CAGR of 5.3% over the forecast period, fueled by the growing adoption of higher ARPU 5G services.

The drivers of mobile data revenue growth include:

- Data Consumption Growth: Rising demand for video streaming, social media, mobile gaming, and other data-intensive services

- 5G Premium Pricing: Higher-margin 5G service packages attracting premium-paying customers

- IoT Applications: Internet of Things services (connected vehicles, industrial IoT, smart home applications) expanding data service opportunities

- Digital Commerce: Mobile commerce platforms generating data traffic through transactions and customer engagement

High-data quotas and premium unlimited plans are further driving revenue growth in the mobile data segment. Operators increasingly emphasize unlimited or very-high-quota data packages as premium offerings, attracting customers willing to pay premium rates for uninterrupted high-speed connectivity.

5. DIGITAL ACCESS AND INTERNET PENETRATION

5.1 Internet User Statistics

At the time of report production, Kepios’s analysis of the latest available data indicated that there were 230 million internet users in Indonesia in October 2025.

This figure represents approximately 82% of Indonesia’s total population. The concentration of internet users in a market of 270 million people reflects both exceptional digital adoption and remaining pockets of digital exclusion—populations in remote areas, lower-income households, and older demographics with limited digital literacy.

5.2 Mobile Internet Speed and Quality

Ookla’s data reveals that the median mobile internet download speed in Indonesia increased by 15.61 Mbps (+53.1 percent) in the twelve months to August 2025. Meanwhile, fixed internet connection download speeds increased by 7.82 Mbps (+24.4 percent) during the same period.

The faster growth in mobile internet speeds relative to fixed-line speeds reflects the strategic priority placed on mobile infrastructure development and the advantages of 4G and emerging 5G technologies.

However, comparative analysis reveals challenges: Indonesia’s 4G download speed of 25.6 Mbps in early 2025 placed the country 86th globally and 13th regionally across South Asia, East Asia, and the Pacific, behind peers like Malaysia and Thailand.

5.3 The Remaining Digital Divide

Despite exceptional connectivity in urban areas, significant digital gaps persist. Rural areas, remote islands, and lower-income communities continue facing connectivity challenges. Infrastructure investments through submarine cables, satellite internet, and public-private partnerships like the Palapa Ring project are helping expand access to remote and underserved areas, but universal connectivity remains an aspiration rather than a realized outcome.

6. MOBILE MONEY, FINANCIAL INCLUSION, AND ECONOMIC TRANSFORMATION

6.1 Mobile as Financial Gateway

For many Indonesians, the mobile phone serves as the primary gateway to financial services. Mobile money platforms enable unbanked populations to access basic financial services: money transfers, bill payments, purchasing of digital goods, and micro-credit.

The penetration of smartphone technology across Indonesian society creates unprecedented opportunities for financial inclusion. Digital payment systems that only function through mobile apps become viable serving mechanisms for populations previously excluded from formal financial sectors.

6.2 E-Commerce and Digital Commerce

Mobile phones have become the primary platform through which Indonesians access e-commerce services. Major platforms like Tokopedia, Shopee, and Lazada have designed their services around mobile-first user experiences, recognizing that desktop access, while important, represents a minority of user interactions.

The evolution of mobile commerce reflects both technological capabilities (smartphones becoming more powerful, internet speeds increasing) and behavioral adaptation (younger generations growing up with mobile-first digital experiences).

6.3 Digital Payment Adoption

Digital payment systems ranging from electronic wallets (e-wallets) to QR-code-based payment systems have proliferated across Indonesia, facilitated by smartphone ubiquity. While cash remains important in many contexts, digital payments have become increasingly common in urban areas and among younger demographics.

7. DIGITAL IDENTITY AND REGULATORY FRAMEWORKS

7.1 Mobile-Based Identity Verification

18.3 million mobile subscribers have undertaken identity verification (KTP-based registration), according to GSMA data. This figure represents subscribers who have registered their mobile subscriptions against official government identification documents.

While this figure represents only approximately 6% of total mobile subscribers, it indicates growing integration between mobile telecommunications and government identity systems—a development with implications for financial inclusion, fraud prevention, and digital governance.

7.2 Contract vs. Prepaid Markets

3.5% of mobile connections operate on contract-basis subscriptions, while the remaining 96.5% operate as prepaid services. This prepaid dominance reflects Indonesian consumer preferences and economic realities: prepaid services require no credit checks and allow precise consumer control over spending, advantages particularly important for lower-income populations.

8. CHALLENGES AND FUTURE OUTLOOK

8.1 Infrastructure Disparities

Despite impressive aggregate statistics, significant disparities exist between:

- Urban and Rural: Major cities have access to cutting-edge 4G and emerging 5G services, while rural areas often experience basic 3G coverage

- Geographic Challenges: The archipelagic geography of Indonesia—over 17,000 islands—creates unique infrastructure challenges, with submarine cables and cellular networks proving expensive to deploy across water barriers

- Economic Disparities: Wealthier populations in major urban centers have access to premium high-speed services, while lower-income populations may access only basic connectivity

8.2 Regulatory Challenges

Indonesia’s telecommunications operators navigate regulatory environments characterized by:

- Spectrum Costs: Historically high spectrum fees constraining operator capital for network investment

- Permitting Complexity: Complex permitting landscapes requiring significant time and resources to deploy new infrastructure

- Fragmented Spectrum Allocations: Past spectrum auctions resulting in holdings that, while broadly competitive, remain less efficient than consolidated allocations

The government’s 2025-2029 digital roadmap addresses these challenges through spectrum fee reductions and regulatory modernization.

8.3 Competition and Market Maturation

Indonesia’s mobile telecommunications market shows signs of maturation: growth rates in subscriber numbers stabilizing, competition intensifying, operators shifting from subscriber acquisition to revenue optimization through premium services.

Looking ahead, market growth will increasingly depend on:

- 5G Adoption: Premium 5G services driving revenue growth even as subscriber growth stabilizes

- Non-Voice Services: Data services, IoT applications, and content-based offerings supplementing traditional voice revenue

- Rural Expansion: Extending connectivity to underserved populations, both expanding the addressable market and fulfilling equity objectives

- Adjacent Businesses: Operators expanding into content services, fintech platforms, and digital services beyond traditional telecommunications

9. THE MACROECONOMIC SIGNIFICANCE OF MOBILE CONNECTIVITY

9.1 The Digital Economy Foundation

Indonesia’s digital economy depends fundamentally on mobile connectivity. E-commerce platforms, digital payment systems, social media networks, and online services all depend on accessible, affordable mobile internet.

The penetration of smartphone technology and 4G connectivity has created preconditions for rapid digital economy growth. E-commerce platforms that functioned minimally in 2010 have become national economic forces by 2026, supported by mobile infrastructure that makes online shopping accessible to consumers across Indonesia.

9.2 Employment and Gig Economy Opportunities

Mobile connectivity has enabled gig economy platforms (ride-sharing, food delivery, freelance services) that create employment opportunities for millions of Indonesians. These platforms depend entirely on smartphone access and reliable mobile internet connectivity.

9.3 Social and Political Implications

The penetration of smartphones and internet connectivity has transformed Indonesian political and social landscapes. Social media platforms enable grassroots organizing, facilitate electoral participation, and provide mechanisms for civil society engagement—with implications for democracy, political participation, and civic consciousness.

10. GLOBAL CONTEXT AND COMPARATIVE ANALYSIS

10.1 Indonesia in Global Context

Indonesia’s 351 million smartphones represent approximately 10% of all smartphone connections globally. This single nation’s market exceeds the total populations of most countries, highlighting the extraordinary scale of Indonesia’s mobile market.

The GSMA forecasts indicating 32% 5G penetration by 2030 in Indonesia contrast with more aggressive 5G rollouts in developed markets (where 5G adoption is advancing rapidly) and reflect realistic assessments of Indonesia’s infrastructure development pace and economic constraints.

10.2 Regional Leadership

Within Southeast Asia, Indonesia leads in absolute numbers. While penetration rates in smaller countries like Singapore and Malaysia exceed Indonesia’s percentages, Indonesia’s absolute scale makes it the region’s dominant mobile market.

CONCLUSION: INDONESIA’S DIGITAL FUTURE

Indonesia’s 351 million smartphones, 96.4% broadband penetration, and rapidly expanding 5G infrastructure position the nation as a global digital leader. The transformation from a telecommunications market centered on basic voice and SMS services to one dominated by data-centric mobile internet represents one of the most rapid infrastructure transitions in human history.

The challenges remain substantial: geographic dispersion, regulatory complexity, infrastructure disparities between urban and rural areas, and millions of Indonesians still lacking reliable digital access. Yet the trajectory is clear: Indonesia is becoming a fully connected digital nation, and the mobile phone—accessible, affordable, and increasingly powerful—is the technology driving this transformation.

For investors, policymakers, entrepreneurs, and Indonesians themselves, the implications are profound. The market dynamics, infrastructure investments, and regulatory evolution documented in GSMA data and telecommunications industry analysis indicate that Indonesia’s digital future will be shaped by mobile-first technologies, 5G capabilities, and the hundreds of millions of Indonesians accessing digital services through smartphones.

The smartphone has become Indonesia’s primary gateway to modernity, economic opportunity, and digital participation. As Indonesia continues its digital transformation through 2026 and beyond, the mobile phone—connecting 351 million users to each other and to the world—will remain at the center of the nation’s digital evolution.

Sources and References

- GSMA Intelligence – “Indonesia: Prakiraan Penggunaan Seluler 2025” (Indonesia: Mobile Phone Usage Forecasts 2025)

- DataReportal – “Digital 2026: Indonesia”

- GlobalData – “Indonesia Set for Steady Telecom Growth Fuelled by Rising 5G Uptake and FTTH Demand”

- TelecomLead – “Indonesia Telecom Market Outlook: What 5G, Faster Internet, and Fiber Expansion Mean for Consumers”

- TelecomTV – “Indonesia Set for Steady Telecom Growth Fuelled by Rising 5G Uptake and FTTH Demand”

- Opensignal – “Indonesia in Focus: Charting a Path to Network Excellence”

- GSMA Newsroom – “GSMA and Kominfo Showcase the Transformative Power of 5G and Mobile Technologies”

- GSMA Intelligence – “The Mobile Economy 2025”

- GSMA Intelligence – “Accelerating 5G in Indonesia: A Spectrum Roadmap”

This article documents Indonesia’s mobile telecommunications landscape as of June 2026, synthesizing data from GSMA Intelligence, telecommunications industry analysis, and official operator announcements reflecting market conditions through Q3 2025 and early 2026.

Disclaimer: This article is journalistic analysis based on telecommunications industry data, government policy announcements, and operator financial reports as of June 13, 2026.