THE RISING TIDE OF FRAUD IN INDONESIA: A DIGITAL CRISIS DEMANDING URGENT ACTION

As card fraud, identity theft, and cyber-scams explode across the archipelago, Indonesia faces a trillion-rupiah crisis that threatens financial stability and consumer confidence

INTRODUCTION: A NATION UNDER SIEGE FROM DIGITAL FRAUD

Indonesia is experiencing an unprecedented surge in financial fraud, with devastating consequences for millions of citizens and the nation’s digital economy. Indonesia recorded Rp7.9 trillion ($474 million) in losses from online scams between November 2024 and November 2025, marking a catastrophic drain on household savings, business capital, and public trust in financial institutions.

The crisis extends far beyond isolated incidents. Approximately 65% of Indonesians received fraudulent calls or texts at least once a week in 2024, creating a pervasive climate of fear and uncertainty that affects virtually every segment of society. For a nation of over 270 million people with rapidly growing digital adoption, this represents not merely a security challenge but an existential threat to the viability of Indonesia’s digital transformation.

The problem is multifaceted and evolving. Card fraud, identity theft, phishing scams, deepfake exploitation, account takeover attacks, and organized investment fraud schemes operate in a complex ecosystem where criminals leverage advancing technology to outpace defensive measures. Government agencies, financial institutions, and security experts are engaged in a frantic race to contain a crisis that shows no signs of slowing.

1. THE ANATOMY OF FRAUD IN INDONESIA: UNDERSTANDING THE EPIDEMIC

1.1 The Scope and Scale of the Crisis

The statistics paint a grim picture of a nation struggling to protect its citizens from sophisticated financial crimes. Indonesia’s financial sector faces rising fraud challenges driven by rapid digitization, with losses from credit card fraud, identity theft, and online scams increasing by 35% annually. This upward trajectory suggests the crisis is accelerating rather than stabilizing.

Direct financial losses reached an estimated $2.1 billion in 2024 across Indonesia’s banking, insurance, and fintech sectors. These are not abstract figures divorced from human suffering—they represent the life savings of retirees, the education funds of families, the startup capital of entrepreneurs, and the operational budgets of small businesses.

The human cost is equally staggering. Individual victims lose an average of 18 million rupiah per incident, a sum that represents months of earnings for many Indonesians. For vulnerable populations with limited financial literacy and modest savings, a single fraud incident can be catastrophic—triggering cascading debt, loss of housing, or abandonment of essential services.

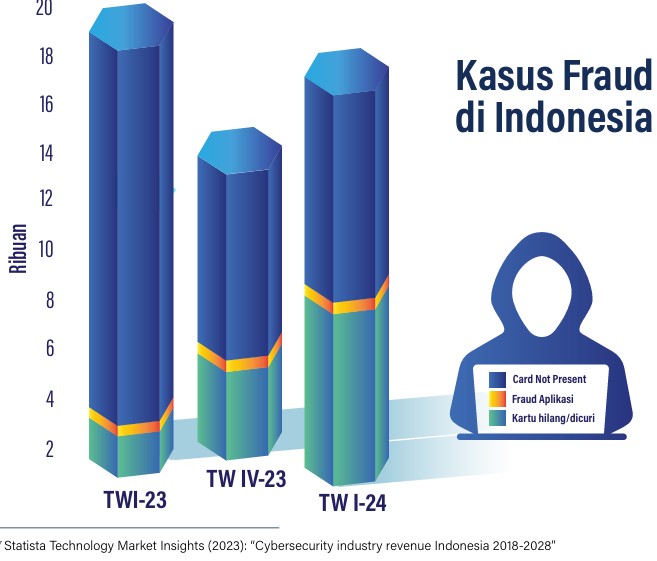

1.2 The Three Pillars of Fraud: Card-Based, Application, and Theft

The data presented in recent statistics reveals three primary categories of fraud that plague Indonesian consumers and financial institutions:

Card Not Present (CNP) Fraud: This category encompasses fraudulent transactions where the physical credit or debit card is not presented—transactions conducted online, over the phone, or through mail order. CNP fraud has become increasingly common as e-commerce adoption accelerates across Indonesia.

Fraud Aplikasi (Application Fraud): This category includes fraudulent applications for credit products, loans, insurance policies, and other financial services where criminals use false identities, forged documents, or synthetic identities to obtain credit.

Kartu Hilang/Dicuri (Missing or Stolen Cards): This traditional form of fraud occurs when physical payment cards are lost or stolen and used by fraudsters before the legitimate cardholder can report the loss.

The relative proportions of these fraud types have shifted over time. Data tracking from Quarter 1 2023 through Quarter 1 2024 reveals trends in how fraudsters are adapting their tactics and which vectors offer the most profitable opportunities for criminal exploitation.

1.3 Geographic Concentration and Regional Vulnerability

Fraud in Indonesia is not randomly distributed—it concentrates in regions with the largest urban centers, highest internet penetration, and most developed financial infrastructure. The provinces with the highest number of reports were West Java (61,857 cases), Jakarta (48,165), East Java (40,454), Central Java (32,492), and Banten (20,619).

This geographic concentration reflects several factors:

Population Density: Major metropolitan areas have higher population densities, providing fraudsters with larger target markets and greater anonymity within urban masses.

Internet Penetration: Urban regions have higher rates of internet and digital payment adoption, creating more transaction vectors for fraud.

Digital Payment Usage: Cities have higher adoption of online banking, e-commerce, and mobile payment systems—exactly the platforms criminals exploit.

Infrastructure: Urban areas have more developed financial infrastructure, more sophisticated criminals, and more organized fraud rings.

Wealth Concentration: Urban areas contain higher concentrations of disposable income and consumer credit, making them more attractive targets for fraud operations.

2. THE SPECIFIC CATEGORIES OF FRAUD DEVASTATING INDONESIA

2.1 Online Shopping Fraud: The Most Prevalent Threat

Online shopping fraud represents the largest category of fraud cases in Indonesia, reflecting the explosive growth of e-commerce adoption across the nation. Online shopping fraud is the most frequently reported scam, accounting for 53,928 cases and resulting in losses of Rp 988 billion, with an average financial impact per victim of Rp 18.3 million.

This form of fraud operates through multiple mechanisms:

Fake Marketplace Listings: Criminals create sophisticated replicas of legitimate e-commerce platforms or post fraudulent listings on established marketplaces, offering non-existent products or counterfeits at artificially low prices.

Non-Delivery After Payment: Consumers transfer payment but never receive merchandise. By the time victims realize they’ve been defrauded, the fraudster’s accounts have been cleared and the money moved through multiple transfers.

Counterfeit Products: Fraudsters deliver counterfeit or significantly inferior products that appear legitimate upon initial inspection but fail upon use.

Bait and Switch: Fraudsters advertise premium products but deliver inferior or unrelated items, exploiting shipping delays that hide the switch until it’s too late to cancel.

Return Fraud: Criminals purchase items using stolen payment methods, then initiate return fraud schemes to obtain refunds while keeping merchandise.

The scale of online shopping fraud reflects Indonesia’s remarkable e-commerce growth. As more Indonesians embrace digital shopping—particularly in regions with limited access to physical retail—the opportunity for fraudsters expands exponentially. The convenience that attracts legitimate consumers also attracts sophisticated criminal networks.

2.2 Impersonation and Fraudulent Calls: The Trust Exploitation Crisis

Impersonation scams represent a particularly insidious form of fraud that exploits the inherent trust within families and communities. Impersonation scams via fake calls have led to 31,299 incidents, with losses totalling Rp 1.31 trillion and an average loss of Rp 42 million per case.

These scams operate on a deeply human level:

Family Emergency Scams: Fraudsters impersonate family members claiming to be in urgent financial distress—medical emergencies, legal troubles, or accident situations requiring immediate payment. The emotional manipulation exploits the victim’s love and sense of familial obligation.

Authority Impersonation: Scammers pose as police officers, tax authorities, or bank officials claiming the victim has violated regulations or is the target of criminal investigation. Fear and intimidation drive immediate compliance without verification.

Romantic Scams: Fraudsters develop elaborate fake romantic relationships over weeks or months, building emotional connections before fabricating crises requiring financial assistance.

Tech Support Scams: Criminals pose as technical support representatives claiming to have detected viruses or security problems on the victim’s computer, then convince victims to grant remote access or purchase fake security software.

The sophistication of these scams has increased dramatically. Phishing, a common form of cybercrime, uses fraudulent messages on social media, email, or websites to gather private data. The National Cyber and Crypto Agency of Indonesia reported a significant 70 percent increase in phishing cases recorded throughout the year compared to 2023.

What makes these scams particularly devastating is their cultural targeting. In many cases, scammers pose as a relative or close friend in distress, such as needing urgent financial help or medical emergencies, resulting in the victim acting quickly without questioning the situation. Criminals have studied Indonesian cultural values—family loyalty, communal responsibility, respect for authority—and weaponized these values against potential victims.

2.3 Fraudulent Investment Schemes: The Promise of Quick Riches

Investment fraud preys on the aspirations of Indonesians seeking to build wealth and secure their futures. Fraudulent investment schemes have been reported 19,850 times, with losses amounting to Rp 1.09 trillion and an average of Rp 52 million per victim.

These schemes typically follow a predictable pattern:

Unrealistic Promise: Fraudsters promise extraordinarily high returns—20%, 30%, or 50% monthly returns—that far exceed legitimate market opportunities.

Social Proof Fabrication: Fake testimonials and manufactured “success stories” convince potential investors that others have profited from the scheme.

FOMO Exploitation: Scammers create artificial scarcity and urgency, claiming limited investment spots are available or that early investors receive premium returns.

Withdrawal Blocking: Initial investors receive legitimate returns (paid from new investor money, not genuine profits), encouraging larger reinvestments. When victims attempt to withdraw principal, processing delays and fees appear, ultimately preventing withdrawal.

Collapse: Once the incoming new investor capital proves insufficient to pay promised returns to earlier investors, the entire scheme collapses and the fraudster disappears with accumulated funds.

The appeal of investment fraud is particularly powerful in Indonesia, where:

- Traditional savings accounts offer minimal interest rates

- Legitimate investment products are poorly understood by many consumers

- Desire for wealth creation is intense but opportunities are limited

- Trust in unofficial investment channels is sometimes higher than trust in formal financial institutions

3. THE EMERGING THREAT OF AI-POWERED AND DEEPFAKE FRAUD

3.1 Deepfake Fraud: The 1550% Explosion

One of the most alarming fraud trends in Indonesia involves deepfake technology—AI-generated fake videos, audio, and images designed to impersonate real people. Deepfake fraud jumped by 1550% during the same period between 2022 and 2023 in Indonesia, representing one of the fastest-growing fraud categories globally.

Deepfakes create unprecedented challenges for fraud detection because they bypass traditional identity verification mechanisms:

Facial Recognition Defeat: Deepfake videos can defeat facial recognition systems used for identity verification in banking apps and online services.

Voice Cloning: Criminals can now replicate voices with remarkable accuracy, potentially fooling voice-based authentication systems and deceiving victims in phone conversations.

Behavioral Impersonation: AI-generated videos can replicate not just appearance and voice, but also behavioral patterns and mannerisms.

Authority Exploitation: Deepfakes of government officials, bank executives, or celebrities can be weaponized to issue official-seeming orders or endorsements.

The scale of the deepfake problem is difficult to overstate. Deloitte projections suggest that deepfake fraud losses could reach tens of billions of dollars globally by 2027. In Indonesia, where digital literacy remains uneven and verification mechanisms are less sophisticated than in developed nations, the vulnerability to deepfake fraud may be proportionally higher.

3.2 Account Takeover: The Epidemic of Unauthorized Access

Account takeover attacks, where criminals gain unauthorized access to legitimate accounts and conduct fraudulent transactions, represent a growing threat. In 2024, 97% of businesses in Indonesia faced account takeover attempts.

Even more alarming than the prevalence is the sophistication. Account takeover attacks now employ:

Credential Stuffing: Automated attacks using credentials from previous data breaches to test millions of account combinations.

Phishing and Social Engineering: Manipulating users into voluntarily revealing credentials.

SIM Swapping: Fraudsters convince telecom providers to transfer phone numbers to fraudster-controlled devices, enabling two-factor authentication bypass.

Malware and Keylogging: Installing malware that captures passwords and authentication credentials.

Third-Party Breach Exploitation: Leveraging compromised data from other companies’ breaches to access accounts.

4. IDENTITY THEFT AND SYNTHETIC FRAUD: THE INVISIBLE EPIDEMIC

4.1 The Weaponization of Personal Data

Indonesia faces a severe identity theft crisis where criminals use stolen personal information to commit fraud that can take months or years for victims to discover.

Identity theft and document forgery are significant threats, where individuals unknowingly become legally bound by contracts they never signed. Between 2022 and 2023, identity theft and document forgery fraud globally increased by 20%.

The Indonesian context makes identity theft particularly dangerous:

Limited Verification Standards: Many lending institutions and service providers have inconsistent identity verification standards, making it easier for fraudsters to use stolen identities.

Data Breach Proliferation: Multiple Indonesian companies have suffered data breaches, exposing millions of citizens’ personal information to criminals.

Synthetic Identity Fraud: Criminals combine real personal identification numbers with fabricated biographical information to create entirely new identities that appear legitimate.

Credit Product Fraud: Criminals use stolen identities to apply for credit cards, loans, and fintech products, running up debts that legitimate owners must contest and rectify.

4.2 The Cascading Consequences of Identity Theft

The impact of identity theft extends far beyond immediate financial loss:

Credit Damage: Victims discover fraudulent accounts years later, with destroyed credit histories that impede their ability to obtain legitimate credit for years.

Legal Complications: Victims may face legal liability for contracts signed in their name by fraudsters.

Psychological Trauma: Discovering that one’s identity has been stolen and exploited creates lasting psychological distress.

Financial Rehabilitation: Victims often spend years and substantial resources attempting to clear fraudulent accounts and rebuild credit.

5. THE REGULATORY RESPONSE AND GOVERNMENT ANTI-FRAUD EFFORTS

5.1 The Indonesia Anti-Scam Center: A Step Forward

In response to the escalating fraud crisis, Indonesia’s Financial Services Authority (OJK) established the Indonesia Anti-Scam Center (IASC) on November 22, 2024, representing a coordinated governmental response to the epidemic.

Between November 2024 and October 2025, online fraud losses reached Rp7 trillion (around US$418.5 million), with only Rp367 billion recovered, a mere 5.4% of total losses. During this period, 125,217 victims reported scams to the Indonesia Anti-Scam Center, while another 171,791 cases were reported through financial service providers. Authorities also identified 483,695 suspicious accounts, of which 93,819 have been blocked.

The IASC’s establishment represents acknowledgment of the crisis’s severity and the need for a centralized response. However, the recovery rate of only 5.4% underscores the challenges in combating fraud once it has occurred—prevention and early intervention are far more effective than post-fraud recovery.

5.2 Enforcement Actions and Account Blocking

Government authorities have been implementing increasingly aggressive enforcement measures:

Indonesia’s Financial Services Authority (OJK) said it had prevented losses of Rp376.8 billion (around US$22.7 million) from fraud cases over the past 12 months. Data from the Indonesian Anti-Scam Center (IASC) showed that between November 22, 2024, and October 16, 2025, more than 299,000 reports were received, with total losses estimated at around Rp7 trillion. A total of 94,344 bank accounts were blocked, amounting to Rp376.8 billion.

While these enforcement actions represent progress, the sheer volume of fraud cases—299,000 reports in a single year—illustrates the scale of the challenge. For every account blocked, numerous others remain active, and new fraudster accounts are created constantly.

5.3 Regulatory Evolution and Legal Frameworks

Indonesia has been modernizing its legal frameworks to address emerging fraud threats. Indonesia has enacted Law No. 11 of 2008 on Electronic Information and Transactions (EIT Law), which has now undergone its second amendment through Law No. 1 of 2024, expanding the legal arsenal for combating cybercrimes.

However, regulatory evolution often lags behind criminal innovation. By the time laws are updated, fraudsters have already devised new techniques to circumvent protections. This perpetual game of catch-up means regulations will always be somewhat behind the threat landscape.

6. THE BUSINESS IMPACT: REPUTATIONAL DAMAGE AND INSTITUTIONAL EROSION

6.1 Customer Trust as a Fragile Commodity

Financial institutions face not merely direct fraud losses but catastrophic reputational damage when customers lose confidence in their security measures.

Reputational damage can be catastrophic for financial institutions. A single major fraud incident can trigger customer exodus, with affected banks reporting 25-40% deposit withdrawals within weeks. Rebuilding trust takes years and requires significant marketing investment.

For Indonesian banks already competing with fintech startups and digital wallets for customer attention, fraud-related reputational damage represents an existential threat. Customers may switch to competitors perceived as more secure or may abandon traditional banking entirely in favor of alternative financial services.

6.2 Regulatory Penalties and Compliance Costs

Beyond reputational damage, financial institutions face severe regulatory consequences for fraud prevention failures:

Regulatory penalties from the Financial Services Authority (OJK) can reach billions of rupiah, plus mandatory remediation costs. Non-compliant institutions may face license suspensions or revocations in severe cases. Institutions receive risk ratings that determine examination frequency. Enforcement authority allows OJK to impose sanctions ranging from written warnings to license revocations. In 2024, OJK issued 147 enforcement actions related to fraud prevention deficiencies.

These regulatory penalties create powerful incentives for banks to invest in fraud prevention, yet the investment requirements are substantial and the challenges immense.

7. THE VULNERABILITY LANDSCAPE: WHY INDONESIA REMAINS AT RISK

7.1 Digital Literacy and Consumer Awareness Gaps

Indonesia’s rapid digitalization has occurred faster than corresponding growth in digital literacy and fraud awareness. Many Indonesians—particularly in rural areas and among older populations—are adopting digital financial services without adequate understanding of security risks.

Fraudsters exploit these knowledge gaps through social engineering, impersonation, and manipulation tactics that would be immediately obvious to more digitally literate populations.

7.2 Systemic Vulnerabilities in Financial Infrastructure

Indonesian financial institutions often lack the sophisticated fraud detection systems employed by developed-nation banks. Losses from credit card fraud, identity theft, and online scams increase by 35% annually, suggesting that defensive measures are not keeping pace with evolving criminal tactics.

Integration between banks, government agencies, and other institutions remains incomplete. Fragmented systems mean fraudsters can exploit inconsistencies and gaps in information sharing.

7.3 The Organized Crime Dimension

Fraud in Indonesia is not merely individual criminal activity—sophisticated organized fraud rings operate with military-like coordination:

- Network Graph Analysis: Criminal networks map relationships between fraudsters, shared accounts, devices, and transaction patterns

- Division of Labor: Specialized teams handle different fraud components—identity theft specialists, technical hackers, social engineers, money movers

- International Coordination: Many fraud rings operate across multiple countries, exploiting jurisdictional complications that hamper law enforcement

These organized operations dwarf the resources available to law enforcement and regulatory agencies.

8. THE PATH FORWARD: MULTI-STAKEHOLDER SOLUTIONS

8.1 Technology-Based Prevention

Effective fraud prevention requires sophisticated technological solutions:

Artificial Intelligence and Machine Learning: Predictive analytics can identify fraud patterns before transactions complete. By analyzing historical fraud cases, AI models identify early warning signals. When a new account exhibits behaviors matching previous fraud patterns during the first week, the system elevates monitoring intensity.

Natural Language Processing: Natural language processing (NLP) examines unstructured data like customer service conversations, email communications, and social media activity. If a customer suddenly claims their card was stolen but their communication patterns seem scripted or rushed, NLP flags the claim for investigation.

Network Analysis: Network graph analysis maps relationships between accounts, devices, and transactions, revealing organized fraud rings where multiple synthetic identities connect.

8.2 Regulatory and Policy Interventions

Government action is essential:

- Enhanced Identity Verification Standards: Mandating consistent identity verification standards across financial institutions

- Data Breach Notification Laws: Requiring companies to notify customers of data breaches within specific timeframes

- Account Freezing Authority: Enabling rapid account freezing upon fraud suspicion

- International Cooperation: Coordinating with law enforcement agencies in other countries to pursue transnational fraud rings

8.3 Consumer Education and Awareness

Public awareness campaigns must educate Indonesians about fraud tactics:

- Recognizing Phishing: Teaching consumers to identify fraudulent communications

- Password Security: Emphasizing strong, unique passwords and multi-factor authentication

- Verification Procedures: Training consumers to verify caller identity and suspicious requests

- Reporting Mechanisms: Making consumers aware of reporting options and support services

9. THE ECONOMIC AND SOCIAL IMPLICATIONS OF ESCALATING FRAUD

9.1 Macroeconomic Impact

The aggregate fraud losses have macroeconomic implications:

- Reduced Consumer Spending: Fraud victims reduce consumption, dampening economic growth

- Reduced Investment in Digital Financial Services: Citizens fearing fraud avoid digital banking, slowing financial inclusion

- Capital Diversion: Resources that could drive innovation and growth are instead devoted to fraud prevention and recovery

- Inflation of Financial Services: Fraud losses are incorporated into service fees, increasing costs for all consumers

9.2 Social Inequality Amplification

Fraud disproportionately affects vulnerable populations:

- Low-Income Victims: Those with limited savings cannot recover from fraud losses

- Elderly Populations: Older Indonesians are particularly susceptible to impersonation and social engineering scams

- Rural Communities: Less sophisticated fraud prevention in rural financial services makes these populations vulnerable

- Informal Sector Workers: Those without formal bank accounts may be exploited through alternative financial services with inadequate fraud protection

10. LOOKING AHEAD: THE FUTURE OF FRAUD IN INDONESIA

10.1 Emerging Threats on the Horizon

The fraud landscape continues to evolve:

Quantum Computing Threats: Future quantum computers could break encryption protocols currently protecting financial transactions.

Advanced Deepfakes: As AI technology improves, deepfake detection becomes increasingly difficult.

Decentralized Finance Fraud: As Indonesians adopt cryptocurrency and decentralized finance, new fraud vectors will emerge.

Cross-Border Regulatory Arbitrage: Criminals will continue exploiting differences in regulation and enforcement between countries.

10.2 The Critical Need for Collective Action

Addressing Indonesia’s fraud epidemic requires coordinated effort across:

- Financial Institutions: Enhanced fraud detection systems, customer verification, and security protocols

- Government Agencies: Effective enforcement, regulatory oversight, and international cooperation

- Technology Companies: Providing secure platforms and responsible innovation

- Consumers: Maintaining vigilance and adopting security best practices

- Civil Society: Raising awareness and advocating for stronger protections

The statistics are sobering, but they also represent a call to action. Indonesia stands at a crossroads where the trajectory of digital fraud will be determined by the collective response to this crisis.

CONCLUSION: THE STAKES COULD NOT BE HIGHER

This is a serious threat to public safety and public trust. Indonesia must intensify efforts to prevent scams, according to government officials overseeing the anti-fraud response.

The data paints a clear picture: Indonesia is experiencing a fraud epidemic of historic proportions. Rp7.9 trillion in losses. Millions of fraud reports. Thousands of fraudsters operating with impunity. A population living in fear of the next call, the next text message, the next seemingly legitimate online transaction that could drain their savings.

Yet this crisis also represents an opportunity—an opportunity for Indonesia to implement world-class fraud prevention systems, to modernize its financial infrastructure, to educate its citizens, and to demonstrate that a developing nation can compete with the most sophisticated fraud ecosystems in the world.

The question is whether Indonesia will rise to this challenge with the urgency and resources it demands. The stakes—measured in trillions of rupiah, millions of victims, and the viability of Indonesia’s digital future—could not be higher.

Sources and References

- Bloomberg – “Pakistan PM Expects US-Iran Deal to Be Finalized in 24 Hours”

- OJK Financial Services Authority – Indonesia Anti-Scam Center (IASC) Data 2024-2025

- OpenGov Asia – “Indonesia Strengthens Consumer Protection Against Digital Fraud”

- Insurance Business Asia – “Indonesia’s Financial Services Authority Warns of Growing Digital Scam Losses”

- ANTARA News – “Indonesia’s OJK Prevents $23 Million in Fraud Losses in One Year”

- Jakarta Globe – “Online Scams Drain $474 Million from Indonesians in a Year, OJK Says”

- 360info – “With Rising Phishing Scams, Indonesia Needs Regulatory Change”

- Sumsub – “Fraudlympics 2024: Global Fraud Leaderboard”

- FlagRight – “Fraud Detection in Indonesia’s Financial Sector”

- VIDA Indonesia – “Four Emerging AI-Generated Fraud in Indonesia”

- Taylor & Francis Online – “Cybercrime in the New Criminal Code in Indonesia”